Can the Horn of Africa Shoulder the Weight of Global Oil Security?

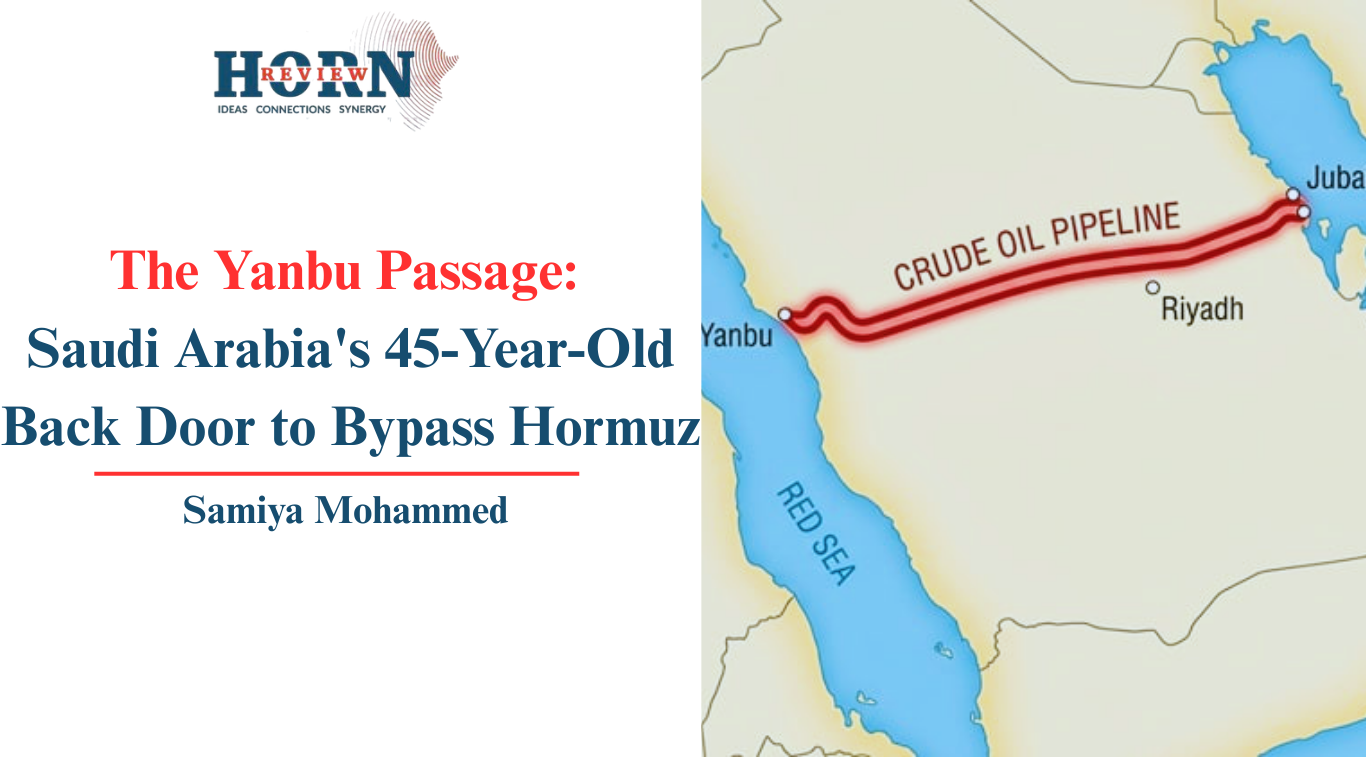

As the conflict with Iran renders the Strait of Hormuz a semi permeable barrier rather than a reliable maritime highway the global energy has been redrawn around a single piece of desert infrastructure. With super tankers idling in the Persian Gulf and insurance premiums skyrocketing Saudi Arabia has activated its Plan B with maximal urgency. Aramco CEO Amin Nasser confirmed in early March that the East West Pipeline often referred to as Petroline would hit its full capacity of 7 million barrels per day in the next couple of days rerouting the orgone of the global economy from the Gulf coast to the Red Sea terminal at Yanbu. This 1,200 kilo meter constructed in 1981 as a hedge against the very scenario now has effectively decoupled Saudi exports from Tehran’s direct control. However while the pipeline is a logistical triumph, it is also a geopolitical rerouting of risk. It does not eliminate the vulnerability of maritime passage ways it just transfers that dependency from one narrow strait to another the Bab el-Mandeb entangling Saudi oil security with the politics of the Horn of Africa and the proxy ambitions of Iran.

The activation of the East-West Pipeline constitutes the culmination of four decades of foresight. Built during the throes of the Iran-Iraq War the original pipeline was designed to insulate Saudi exports from the Tanker War that plagued the Gulf. Over the years its capacity has been systematically expanded particularly following the 2019 attacks on Abqaiq transforming it from a contingency route into a major export passageway. In the current crisis its value is incalculable. With up to 16-17 million barrels per day of Gulf crude effectively halted the pipeline allows approximately 7 million barrels to bypass the Strait of Hormuz entirely.

The flow westwards has surged maintaining a critical line to European markets via the Suez Canal and the Summed pipeline and to Asia via the longer, more expensive route. In the short term the pipeline preserves a semblance of market stability, proving that the 1981 planners correctly identified the primary threat.

However this relief is predicated on a brittle assumption that the Red Sea remains a secure transit zone. The events of the past weeks suggest this assumption is no longer tenable.

The fundamental trade off of the Yanbu bypass lies in its exposure to the Bab el-Mandeb Strait. While Hormuz is a narrow mouth leading into Gulf, the Bab el-Mandeb is the neck of a funnel through which all Red Sea traffic must pass. Situated between Yemen and the nations of the Horn of Africa this Gate of Tears could become the new frontline in the Iranian confrontation. Houthi military officials have already issued threats of a naval blockade against the United States and Israel with explicit warnings that merchant vessels and warships could be intercepted.

For Saudi oil this is not an abstract security concern but an immediate commercial reality. This could mean that loading schedules at Yanbu indicates that approximately 70-75% of exports are now potentially exposed to Houthi interference. This is because the vast majority of this crude nearly 90% is loaded onto Very Large Crude Carriers. These vessels when fully laden are physically incapable of transiting the Suez Canal and must instead navigate south through the Bab el-Mandeb to reach Asian markets or the Saudi Jazan refinery. The pipeline has successfully sidestepped Iran only to place Saudi exports directly in the path of Iran’s most potent proxy.

This geographical reality forges a direct and often underappreciated political link between the Saudi oil ministry and the states of the Horn of Africa. The security of the Bab el-Mandeb is not just a function of Yemeni stability however it is tied to the posture of the horn countries. These nations control the African littoral of the strait. For Saudi Arabia this means that maintaining the flow of oil from Yanbu now requires a cohesive security planning on the opposite shore where a region characterized by an intense geopolitical competition. The stability of the Horn is no longer a peripheral humanitarian concern for Riyadh however it is a direct variable in the equation of national revenue and global market share.

The potential for a cascading crisis is high. If the Houthis escalate from threats to kinetic action mirroring their 2023-2025 campaigns , the impact on global oil markets would be compounded. While a portion of Yanbu’s traffic estimated at up to 2-2.5 million barrels per day can avoid the southern route by heading north to Egypt’s Ain Sukhna port for transit via the Sumed pipeline hence this is a finite capacity. The remaining millions of barrels already diverted once from Hormuz would face either the risk of attack in the Bab el-Mandeb or the punitive costs of rerouting. The economic shockwaves of such a scenario are quantifiable.

The Saudi East-West Pipeline a 45-year-old investment that has paid dividends in a moment of extreme duress. It successfully insulates the Kingdom’s exports from the immediate grasp of Iranian forces in the Gulf. Yet, in the interconnected system of global energy trade, there is no true escape from geography. The pipeline threads Saudi oil through the Red Sea, a corridor whose southern gate is held by actors aligned with Tehran. The political linkage to the Horn of Africa is now cemented by the flow of crude that are no longer distant diplomatic issues but immediate factors in the security of global supply. As Aramco pushes every barrel possible through the pipeline, the Kingdom has traded the certainty of Iranian proximity in the Gulf for the proxy warfare in the Red Sea.

By Samiya Mohammed, Researcher, Horn Review